Capitalism without price discovery is hardly capitalism. “Free” markets that are dominated overwhelmingly by a government agency are not free markets.

BY SEEKING ALPHA FOR THE INTERNATIONAL CHRONICLES

Capitalism… It’s a word that means everything and nothing. To some, it alludes to a system in which oligarchic owners of capital are allowed to shape the economy in their favor. To others, it’s the natural result of the property rights inherent in a free economy.

The dictionary definition of capitalism is simply an economic system in which a nation’s land, resources, industries, and capital are owned by private individuals and businesses rather than the government. It’s often associated with for-profit business, specifically, but private ownership does not necessarily require a for-profit structure. It does, however, give control over capital and assets, including the income streams generated by them, to their owners or shareholders.

The “stakeholder theory,” which has surged in popularity recently, asserts that the owners or shareholders of capital/assets do not (or should not) have full control of these but rather (should) share control with other stakeholders such as employees, customers, communities, and the environment. Some proponents of stakeholder theory are of the view that this should be a voluntary decision made by owners/shareholders, while others assert that it should be the law of the land, enforced by the government.

So often, economic debates in the popular sphere revolve around this dichotomy between the shareholder and stakeholder theories of capitalism, even if different terminology is used. Sometimes the debate is framed as “free market capitalism” versus “Scandinavian-style socialism.” Of course, there is some influence from Jeremy Corbyn-esque quasi-socialists in the political debate, but the majority fall into either one of the two capitalist camps.

However, there is one economy-altering element at play in today’s world that doesn’t fit well into either shareholder or stakeholder capitalism (or quasi-socialism). Neither theory would inherently predict or prescribe the emergence of this element, and yet it has emerged everywhere, in countries that would fall more into the “shareholder primacy” camp as well as those that adhere to a more stakeholder view.

Quantitative Easing’s Distortion of Capitalism

I won’t belabor the anticipation. Regular readers already know that this relatively new element (historically speaking) is quantitative easing from central banks. The Federal Reserve has created trillions of dollars’ worth of digital money credits over the last decade in order to purchase assets on the open market. Most of the purchases were of federal government Treasuries, which had the effect of reducing the supply and making rates lower than they otherwise would be. A significant minority of purchases were of mortgage-backed securities in an attempt to support the housing market.

Earlier this year, I explained in “Blame The Fed For The Plight of The Average American” how monetary policy stimulus, resulting in ultra-low interest rates, has financially hurt the poor and middle class. People often assume that lower rates give the non-wealthy a boost by making it more affordable to buy a home through a mortgage, buy a car through multi-year financing, etc. But as I explained, ultra-low interest rates have actually lured consumers into spending more and taking on more debt than they otherwise would.

We’ve seen this lately with auto loans. Rather than reign in total spending on vehicles, American consumers have increased their borrowing for car purchases recently as interest rates have fallen. Rather than looking at the total cost, these ultra-low rates induce big-ticket-item buyers to look only at the monthly payment, which may remain unchanged or even fall as the total cost over the long run actually increases.

What’s more, consumers (and dealerships) have stretched out loan terms in order to keep the monthly payments down. Terms lasting longer than six years are a growing part of the auto loan market. Now, it’s true that the average lifespan of cars on the road today is over 11 years, but paying monthly interest for over six years on a depreciating asset seems like a universally unwise financial decision. It results in a total cost well above the purchase price. This is partially why we’ve seen auto debt as a percentage of overall household debt jump from 6% in mid-2009 to 10% today.

Another example of low rates paradoxically hurting the non-wealthy comes from the United Kingdom, in which household debt is “worse than at any time on record” as of 2018.

And, by the way, to the extent that the wealthy are more likely to make big ticket purchases with all cash (no debt) while the non-wealthy are more likely to use financing (debt), the Fed’s monetary policy decisions have exacerbated wealth inequality.

In my article, I also explained how the inflation produced by the Fed’s monetary policies have differing effects on the various income levels. The lower one’s income level, the higher the percentage of that income is spent on utility bills, internet, gas, groceries, rent, cell phones, car notes, etc. The poorest quintile spends over double that of the rich to heat and air condition their homes, for instance. Rising consumer prices for these everyday items are more of a burden for the less well-off than they are for the rich.

Pedro da Costa explains in a recent MarketWatch article that companies producing luxury products for the wealthy are experiencing increasing degrees of competition, and the prices of those goods are growing slower than goods geared toward the non-wealthy.

Meanwhile, the poor and middle class are significantly more likely to have less competition for everyday items such as internet or health insurance providers, resulting in faster price growth. Da Costa’s article is based off a new study from Columbia University’s Center on Poverty & Social Policy, which found that real (inflation-adjusted) income growth from 2004 to 2018 was slower than the official measurements for all but the highest-income quintile.

Source: MarketWatch

And yet, the Fed makes policy decisions based on one inflation measurement that averages consumer price growth for all income groups, ignoring the disparity in how this one metric is experienced by different groups. Whenever that inflation metric begins to dip, presumably reflecting some relief for spenders, the Fed steps in with monetary stimulus in order to give it a boost.

Hence we find the lower half of the income spectrum increasingly opting to shop at discount retailers and grocers such as Walmart (WMT), Costco (COST), Dollar General (DG), Ross (ROST), T.J. Maxx (TJX), and Aldi, where they perceive consumer prices to be more reasonable. Meanwhile, the rich are significantly more likely to benefit from the low-cost products of Amazon (AMZN) via the Prime service, as both their membership and their total spend are higher than lower-income groups.

Here’s the crucial question to ask: Were these economic effects the result of capitalism? Were they the natural consequence of private ownership of capital and assets?

The answer, of course, is no.

If we imagine a world in which monetary policy is much more hands-off, with central bank-set rates following market forces of supply and demand rather than (mostly) the other way around, there would still be some price inflation. There would still be inequality. The rich would still have lower personal debt-to-income ratios than lower-income groups. But there wouldn’t be a powerful government agency making these issues dramatically worse.

Quantitative Easing’s Amplification of Inequality

In this imaginary world of fully market-determined interest rates and little-to-no assets on central bank balance sheets, wealth inequality would be significantly less extreme. And not just for the reasons mentioned above.

Earlier this year, I explained in “Blame (Or Thank) The Fed For Meteoric Wealth Inequality” that stimulative monetary policies that have been pursued since the 1980s have played a huge role in compounding wealth (and, to a lesser extent, income) inequality. Stocks tend to fare better when real interest rates decline, and vice versa. Plus, the savings vehicles preferred by the non-wealthy tend to perform better when real rates are higher, and vice versa. Thus, as real rates have fallen since the 1980s, wealth inequality has soared.

When interest rates hit zero a decade ago, central banks used quantitative easing to continue suppressing rates across the curve. By lowering the supply of safe income assets, this injection of liquidity into the financial system caused rampant yield-chasing activity that boosted the risk assets primarily owned by the rich. Some of the biggest stock market gains in American history occurred during the Fed’s large-scale asset purchases. By making risk asset returns more attractive compared to safe asset yields, QE manipulated the price signals that would otherwise have determined the performance of those assets.

Furthermore, corporations took advantage of ultra-low costs of debt to increase their debt loads while buying back record amounts of their own shares, further boosting profitability and stock prices.

The result? According to the Congressional Budget Office (via Stephen Roach), “virtually all of the growth in pre-tax household income over the QE period (2009 to 2014) occurred in the upper decile of the US income distribution, where the Fed’s own Survey of Consumer Finances indicates that the bulk of equity holdings are concentrated.”

As pointed out by Sven Henrich, the latest round of Fed balance sheet expansion, just like prior iterations, has rendered the market void of intraday price discovery, pushing stocks on a one-way journey upward. It has decoupled stock prices from fundamentals and driven investors into “extreme greed” territory, according to CNN’s Fear & Greed Index.

Source: CNN

Regardless what Fed officials want to call it, this central bank balance sheet expansion has resulted in six straight weeks of upward market movement, with each major index hitting multiple record highs, even while the S&P 500 (SPY) delivers its third quarter of aggregate earnings declines and is expected to hit a fourth in Q4 2019.

Don’t take my (or any market commentator/practitioner’s) word for it. Listen to the Bank of International Settlements, which recently found that central bank stimulus is distorting financial markets.

QE has negatively impacted the functioning of asset markets, the BIS says. “These [negative impacts] included a scarcity of bonds available for investors to purchase, squeezed liquidity in some markets, higher levels of bank reserves and fewer market operators actively trading in some areas.” They also include lower credit spreads among this list.

Source: Financial Times

According to the BIS, “Negative impacts have been more prevalent when central banks hold a larger share of outstanding assets.” In other words, as central bank balance sheets grow as a percentage of the economy, these negative impacts will have correspondingly greater effect.

A question springs to mind about a recent anomaly in the Fed’s wheelhouse. What caused the spike in overnight rates a few months ago? In short, banking regulations force large banks to hold a certain amount of liquidity, which prevented them from lending en masse during the brief rate spike. Lending at mid-single-digit rates in the overnight market should have been attractive for any market participant, but the banks themselves said they didn’t do it due to the constraints of liquidity regulations.

Now, the point here is not to make a claim about the efficacy or prudence of certain banking regulations, but rather to ask: Is this capitalism? Is something inherent in capitalism broken to cause these negative impacts on the financial markets?

Again, the answer is no. Capitalism without price discovery is hardly capitalism. “Free” markets that are dominated overwhelmingly by a government agency are not free markets.

The Reigning Monetary Regime’s Effect On Stock Valuations

Lance Roberts & Michael Lebowitz recently provided an insightful commentary on the Shiller CAPE ratio:

“This ratio, which is the price of the market divided by the 10-year average of trailing earnings, has been widely discussed in the media, and often dismissed during bull market advances, because of it does not timely signal turning points in the market.

The chart below tells a simple story. When valuations are elevated (red), forward returns have been low and market corrections have been exceptionally deep. When valuations are cheap (green), investors have been handsomely rewarded for taking on investment risk.”

Source: Real Investment Advice

But you will notice an issue with using historically high (greater than 20) readings of the CAPE as an indication of market overvaluation: by this measurement, the S&P 500 has been overvalued for the better part of the last three decades! There have been no undervalued times to buy into the index since the early 1980s. In fact, there’s only been one period in the last thirty years of even average valuation – during the doldrums of the Great Recession.

As Roberts & Lebowitz put it, “The problem with fundamental measures, as shown with CAPE, is that they can remain elevated for years before a correction, or a ‘mean reverting’ event, occurs.” This was true prior to the late 1980s, but thereafter, the market has been stuck in this lofty position.

The average CAPE valuation from 1900 to 1990 was 14-15, but the average from 1990 to today has been around 24-25. What changed between those two periods? The Greenspan Put.

When the stock market crashed in 1987 on the back of high valuations but a fundamentally strong economy, Fed chairman Alan Greenspan (himself an Ayn Randian free marketeer in philosophy, if not in action) ignored the economic fundamentals and swooped in with monetary easing to cushion the market. As a result, stocks kept their high CAPE multiple instead of reverting to the mean as they had in the past. This happened multiple times, such that Greenspan became termed the “Maestro” of the markets.

Following Greenspan came the Bernanke Put. And then the Yellen Put. And, finally, the Powell Put.

Investors need to come to grips with the fact that ultra loose and accommodating monetary policy has reset the mean to an indefinitely higher level. Readers may raise their eyebrows at that, being reminded of Irving Fisher’s statement in 1929 that the stock market had reached a “permanently high plateau.” But central banks were not the economic force in the 1920s that they are today. They did have an effect, but only fractionally compared to the contemporary regime.

During the currently reigning monetary regime, the stock market has reached unprecedented valuations based on several metrics.

Take the Tobin’s Q ratio, which is the total market capitalization measured against the underlying assets’ replacement value, currently about as high as the tech bubble peak.

ChartData by YCharts

So, also, is total market capitalization measured against GDP, coming in at around 147%.

ChartData by YCharts

Let’s look at one more valuation metric. This one is a bit more obscure: S&P 500 market cap to aggregate net income. Unlike earnings per share, which can be manipulated by share buybacks (which we’ll return to below), net income is a measurement of total profits.

The SPX market cap as of April 30, 2019, was $23.7 trillion. Dividing that by the SPX’s ~$300 billion aggregate net income shows a multiple of 79x. Compare that to the beginning of 2011: $11.2 trillion divided by ~$200 billion in aggregate net income, coming to a 56x multiple.

This record-setting valuation expansion is not the result of the normal fluctuations of the market cycle natural to capitalism. They’re the result of the ever more consequential policy decisions of central banks.

The Financialization of Capitalism

Lastly, let’s zoom in a bit further to examine the distortion of capitalism from a slightly different angle – that of financial engineering or financialization.

By “financialization,” here, I’m referring to the ability of businesses to generate increased profits from the same amount of revenue without increasing productivity. It’s the ability to convert the same amount of sales into a higher amount of earnings without adding additional value to the economy.

“Financialization is profit margin growth without labor productivity growth,” says Ben Hunt of Epsilon Theory. It is the systematic conversion of product and service sales (mainly to the non-wealthy) into expanded profits (enjoyed mainly by the wealthy).

This process happens primarily through two mechanisms: cost cutting and share buybacks.

For most of the history of capitalism, financialization has been limited by some basic factors. On the cost-cutting side, there’s a limit on the amount of costs that can be cut from the production or administrative process before business functioning begins to suffer. In other words, cut costs too much and the ability to continue generating revenue growth will eventually be hindered.

And buybacks have long been limited by prohibitively high costs of capital relative to the shareholder returns that they purchase. In other words, when interest rates floated in a historically normal range, buybacks were mostly impractical due either to the cost of debt or to relatively high investment hurdle rates. As interest rates have fallen, so too have the hurdle rates for corporate investment, incrementally making unproductive uses of capital like buybacks seem like better uses of cash.

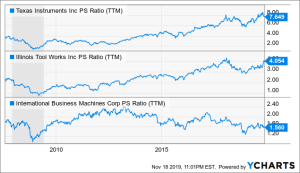

One example of financialization is Texas Instruments (TXN), a semiconductor and technology company. Hunt digs into TXN’s finances from recent years to paint a picture of where the cash flows have gone. Over the last five years, he estimates the company generated roughly $25 billion in free cash flow. About $3.3 billion of that went to capital expenditures, with most of that probably going into maintenance capex rather than growth capex. Another $1.6 billion went to M&A.

Where did the lion’s share go? Dividends and buybacks. The company paid out $9.1 billion in dividends over the five-year span, while share buybacks accounted for $15.4 billion. Combined, the total return to shareholders has come to $24.5 billion – nearly all of FCF. The remaining spending was funded with debt issuance.

Over that five-year period, TXN bought back 228.6 million shares at an average price of $67.37 per share, while it issued 90.8 million shares to employees and board members as compensation at an average $27.51 per share. It’s a revolving door of share existence in which insiders can purchase newly minted shares at discounted prices while a much greater amount of shares are purchased at market prices in order to diminish the float.

Hence we find that revenue has grown at an average annual rate of 4.1%, while diluted earnings per share have risen at an average annual pace of 33.9%.

Texas Instruments

ChartData by YCharts

Meanwhile, since November 2007, just prior to the official onset of the Great Recession, top-line revenue growth has come in at 6.6% while costs have been significantly reduced – especially for cost of goods sold (“COGS”).

ChartData by YCharts

The picture is worse for IBM. The following chart shows how buybacks have been used to cushion sliding revenue. From 2010 to 2015, it translated slight revenue growth into magnificent EPS growth. But since 2015, all it has managed to do is slow the fall.

International Business Machines

ChartData by YCharts

And then, of course, you’ve got the cost-cutting, which has helped, too.

ChartData by YCharts

These are just two examples of a widespread trend across public companies. Cost-cutting may have hindered revenue growth across the economy, but corporations have been able to mask it with increased net income (from cost reductions) and EPS (from buybacks). It’s a system that has massively benefited a few at the expense of the many. Unlike productive uses of capital that expand the total wealth of a country, it merely redistributes an otherwise fixed pie of wealth.

Writes Ben Hunt:

Public companies are managed today to mortgage the future OVER and OVER and OVER again, for the primary benefit of management shareholders and the secondary benefit of non-management shareholders.

This is the reason why CEOs today make about 271 times more than the average worker compared to 1978 when they made only 30 times the average worker. In fact, the average pay of CEOs today is high even for members of the top 0.1% of income earners; the average CEO of a large firm makes 5.3 times the average annual earnings of the 0.1%. It’s the value of the stock options that push corporate execs so far above their wealthy peers.

And yet, this dramatic disparity in pay has not resulted in correspondingly improved fundamentals.

According to the website Multpl, S&P 500 sales are roughly 20% higher today than at their pre-recession peak in 2007, translating into annual growth of 1.67%. Compare this to the peak of earnings in 2006 vs. today, marking total growth of 23.5% or 1.96% per year. From 2009 to today, S&P 500 sales have grown 32%, or 3.2% per year, while EPS has grown 55% or 5.5% per year.

The SPY is trading at a price-to-sales of 2.2x, well above the 1.7x reached in late 2000.

And the SPY’s current price-to-book value of 3.3x is meaningfully above the 2.9x reached prior to the Great Recession.

And yet, SPY price-to-earnings at around 23x is only slightly above the pre-recession peak of 22.4x in November 2007 and well below the bubbly 30s-40s P/Es hit in the late 1990s and early 2000s.

Cost-cutting has expanded profit margins, thus boosting net income, and buybacks have juiced EPS off of the base of boosted net income. Thus, the price of the index appears much cheaper against the engineered EPS than it would be otherwise.

And, again, what has made this financialization not only possible but prevalent? Monetary policy support of asset prices since the Fed chairmanship of Alan Greenspan, including quantitative easing. It’s that simple. There still would have been wealth inequality in lieu of this monetary policy regime, but it would not be nearly as pronounced as it is today. Stocks still would have performed well, but not nearly as well as they have.

This is not capitalism.

It’s something else entirely.

Investor Takeaways

I see three primary takeaways from the preceding analysis.

1. Price-to-sales matters in the long run. When bubbles eventually burst, the stocks typically hurt worst are those with strong sales but little or no earnings. But this most recent multiple expansion run-up is different. In recent years, the number of stocks with strong earnings but weak sales growth have proliferated.

Certainly, the next time the market experiences a significant pullback, those stocks that are richly valued based on strong sales growth but little-to-no profits seem poised for pain. But investors should be cautious about those stocks that are showing strong earnings growth but little-to-no sales growth – Illinois Tool Works, one of my core holdings, included. Looking at price-to-sales is one way to offset this trend.

ChartData by YCharts

2. Consumer-oriented companies increasingly need to “pick a lane,” designing their products to target either the wealthy or the non-wealthy. It would seem intuitive that, eventually, consumer debt would reach a limit such that financing more expensive consumer products becomes impossible or impractical. How expensive do iPhones need to be before consumers hold back on buying? What about Ford (F) trucks? Or sectional couches?

Some of the most successful companies today have definitively “picked their lane” and serve it well, either with their entire business model or with specific products.

3. There’s no telling how high equities can go or how long they can stay elevated with the Fed’s preemptive QE ongoing. This point speaks for itself. To me, it signifies that a balance between continued stock exposure to enjoy the remaining upside and a meaningful cash allocation for dry powder is necessary.